Banking on growth

In Greater Lafayette, lenders are helping finance a period of remarkable expansion while confronting the financial realities of a changing banking industry

For most of the past decade, American community bankers have worried about markets standing still: too little population growth, too little business investment, too little demand for loans. In Greater Lafayette, they face a different conundrum.

The region, anchored by Purdue University and a manufacturing base that includes Subaru, Caterpillar, Wabash and GE Aerospace has spent the last several years generating the kind of commercial activity that financial institutions ordinarily spend considerable effort trying to attract.

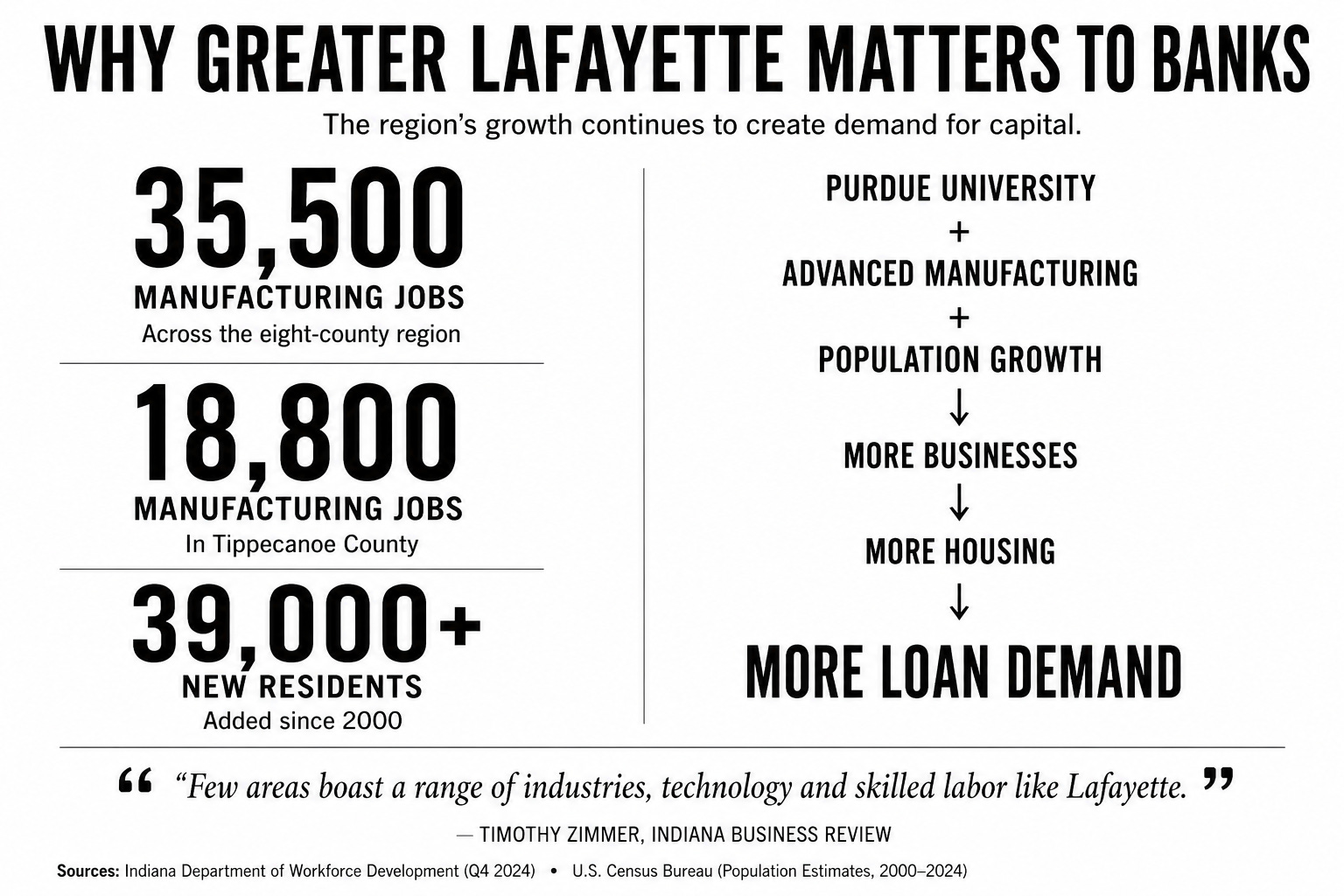

A semiconductor supply chain is forming around Purdue’s research park. A new emergency department is headed to West Lafayette. Industrial parks are filling. Population has grown by roughly 39,000 residents since 2000, and it has not stopped.

Banks are busy. That is not the same thing as banks being comfortable. The institutions competing for Greater Lafayette’s financial relationships are operating in an environment where growth no longer guarantees easy money.

Deposits are more expensive to attract and hold than they were three years ago. Commercial real estate projects require harder scrutiny. Technology costs are rising faster than many smaller institutions budgeted for. And the single largest deposit holder in the market is not a bank at all; it is a credit union founded on a university campus in the late 1960s.

Greater Lafayette is not a troubled banking market. It is a productive one, and productivity, here as everywhere, has extracted its price. The same growth that fills loan pipelines has driven up the cost of the deposits that fund them. The same expanding economy that justifies every branch in Tippecanoe County has made every branch harder to sustain.

The deposit war

For a long time, the money just sat there.

It sat in checking accounts and savings accounts and certificates of deposit, patient and cheap, asking nothing of the institutions that held it. Community banks and regional lenders built their business models around its stillness, funding loans at spreads that felt, in retrospect, almost generous. It was not a strategy so much as a condition, the financial equivalent of good weather, reliable enough that you stopped noticing it.

Then, in 2022, the weather changed.

When the Federal Reserve began raising rates, those deposits started moving into money market funds, Treasury bills, higher-yield accounts at online platforms operated by national banks that never needed a branch in Tippecanoe County to compete for the business.

The FDIC’s Quarterly Banking Profile for the first quarter of 2026, released in late May, showed the industry on solid footing in aggregate — $80.5 billion in net income, a 1.26% return on assets, and domestic deposits rising for a seventh consecutive quarter. But the report also showed industry net interest margin declining eight basis points from the prior quarter to 3.31%, as earning asset yields fell faster than funding costs. For community banks specifically, the yield on earning assets dropped 18 basis points while the cost of funds fell only 12, a six-basis-point squeeze that has become the defining pressure of the current operating environment.

The Conference of State Bank Supervisors’ Annual Survey of Community Banks has tracked this shift in real time. Net interest margins were cited as the most important external risk facing community banks in its most recent results. In the Independent Community Bankers Association’s (ICBA) 2026 CEO Outlook survey, nearly 60% of community bank leaders said growing deposits was their greatest business challenge, a near-reversal from 2022, when most said the challenge was finding borrowers for the flood of pandemic-era deposits on their books.

The rate cycle permanently reshuffled how banks, investors and analysts think about deposit quality.

“Deposits represent the true value of a banking franchise. What that means in practice is that not all deposits are equal — institutions with high concentrations of low-cost, stable accounts now command premium valuations over those that had to pay up to keep money on their books,” said Nathan Stovall, director of financial institutions research at S&P Global Market Intelligence in a 2025 analysis of community bank deposit franchises.

In Greater Lafayette, that competition is playing out in a market unusually dense for a community of its size. Forty-four branches of 17 banks serve Tippecanoe County, according to the FDIC's Summary of Deposits as of June 30, 2025, not counting credit union locations operated by Purdue Federal and IFCU, which do not appear in FDIC deposit tallies.

Total bank deposits in Tippecanoe County stood at $3.9 billion. The broader Lafayette Metropolitan Statistical Area (MSA), which spans multiple counties, carries a larger deposit pool — First Merchants has cited a figure of roughly $14 billion in its investor materials — but the county figures are the most precise apples-to-apples comparison available.

No bank in Greater Lafayette holds more deposits than Purdue Federal Credit Union

Before any bank is counted, the largest deposit holder in Greater Lafayette is Purdue Federal Credit Union.

Organized on the Purdue campus in 1969 and headquartered in West Lafayette, the credit union holds $1.802 billion in total shares and deposits, according to its most recent quarterly financial filing with the National Credit Union Administration. That figure does not appear in FDIC deposit data, which excludes credit unions entirely — but it exceeds the county deposits of JPMorgan Chase, First Merchants, and every other bank in the market. Purdue Federal’s $1.802 billion outpaces Chase’s $1.163 billion by $639 million.

Its financial profile is strong. The net worth ratio stood at 10.9% at year-end 2025, above the federal well-capitalized floor of 7% and near the national credit union median. It carries $225.5 million in net worth against $2.1 billion in total assets, $1.52 billion in loans, and a delinquency rate on balances 60 days or more past due of less than 0.2%. Its 111,039 members span 13 locations across Greater Lafayette, Crown Point and La Porte.

That capital funds competitive pricing. The credit union’s member-giveback program returned $7.6 million to members in the most recently reported full year — a direct offer to any faculty member, staff employee or Purdue-affiliated contractor choosing where to bank. As Cherry Bekaert noted in its 2026 banking report, credit unions have become increasingly active acquirers of banks, with target assets hitting their highest annual total ever in 2024. Purdue Federal doesn’t need to acquire anyone. It is already larger than any bank in this market, and it is growing.

Among banks, Chase holds nearly 30% of the market

Somewhere along the way, a threshold was crossed. The institution that came to hold more deposits in Tippecanoe County than any other was not the one with the longest history here, or the deepest knowledge of the market, or the most familiar name on a downtown marquee. It was JPMorgan Chase, a bank that, for most practical purposes, was already in Lafayette before it arrived.

According to the FDIC Summary of Deposits as of June 30, 2025, Chase held $1.163 billion in Tippecanoe County deposits across three branches — a 29.75% share of the county bank market, nearly seven percentage points ahead of the next largest institution. That is a striking concentration for a $4 trillion bank whose Greater Lafayette presence is three branches.

The explanation is structural. Purdue University enrolls more than 50,000 students, a significant share of whom arrive with Chase accounts established in their home markets and never switch. Faculty and staff recruited nationally bring the same inertia. A Purdue professor with a Chase account from a previous city does not automatically leave it when they move to West Lafayette. That accumulated loyalty, replicated tens of thousands of times, is how a bank with no particular roots in Lafayette comes to hold more local deposits than any institution that has been here for decades.

Chase competes in the market largely on brand recognition, digital infrastructure and the sheer weight of an existing customer base. Its deposit dominance is less a statement about local banking relationships than about how national scale moves money and stays put.

First Merchants bets on scale

The dominant commercial lender in Tippecanoe County is First Merchants Bank, the retail arm of Muncie-based First Merchants Corporation, which trades on the Nasdaq under the ticker FRME.

The bank operates six branches across the Lafayette-West Lafayette area, more than any other locally-rooted institution in the market and held $888.2 million in Tippecanoe County deposits as of June 30, 2025, a 22.73% share and the second-largest position in the county, according to FDIC Summary of Deposits data.

The bank’s answer to that competitive pressure has been to get bigger. In September 2025, First Merchants announced a $241.3 million all-stock deal to acquire First Savings Financial Group, a southern Indiana lender headquartered in Jeffersonville, and closed it on February 1 of this year. The transaction added $2.4 billion in assets and $1.7 billion in deposits — giving the combined institution a balance sheet of $21.1 billion and a statewide footprint that now stretches from the Wabash Valley to the Louisville suburbs.

The first quarter of 2026 showed what that kind of growth costs before it pays off. Reported net income fell to $27.7 million from $54.9 million a year earlier, weighed down by $17 million in acquisition charges and a $29.8 million loss on low-coupon mortgage loans reclassified for sale.

But those are one-time items, and the underlying business told a different story: adjusted earnings per share rose 9.6% over the prior year, net interest margin climbed to 3.35%, and management projected continued improvement through the end of 2026 as integration costs burn off.

The strategy reflects a calculation playing out at regional banks across the country. Cherry Bekaert’s 2026 Banking Industry Report found that the largest banks’ technology budgets now exceed those of regional institutions by a factor of 10, a gap that widens every year. More than 180 bank deals were announced nationally in 2025, the highest count since 2021, according to Ankura’s banking industry outlook, as mid-sized institutions concluded that the cost of staying independent was rising faster than the cost of merging.

A larger balance sheet means larger lending limits, a broader product shelf and more capital to spend on the technology that customers increasingly expect.

On the April earnings call, Mark Hardwick, First Merchants’ chief executive officer, sounded confident about what comes next.

“It’s very pleasing to see our Midwest economy continuing to expand, our clients’ businesses continuing to grow, and our bankers continuing to win new relationships,” he told analysts.

He projected mid-single-digit loan growth through the end of 2026.

Old National: The market’s fourth-largest depositor

Old National Bank has been in Greater Lafayette since March 2009, when it completed the acquisition of Charter One’s Indiana retail branch network — 65 locations statewide, including in-store branches in the Lafayette market. In 2014 it moved more decisively into the market, acquiring LSB Financial Corp. and its subsidiary Lafayette Savings Bank — the largest bank ever headquartered in Lafayette, founded in 1869 — for $42 million. The deal added five full-service Tippecanoe County branches and $312 million in deposits, more than doubling Old National’s local presence.

As of June 30, 2025, Old National held $304.9 million in Tippecanoe County deposits across three branches, a 7.80% share, ranking it fourth in the county behind Chase, First Merchants and Centier, according to FDIC Summary of Deposits data. Today Old National competes here as a national institution with 250 locations across eight states and roughly $72 billion in total assets.

Its full-year 2025 results reflect an organization well past its own consolidation phase: net income of $653.1 million, a net interest margin of 3.65% — 30 basis points above the national industry average — and an adjusted efficiency ratio of 46%, among the best in its peer group.

“Our 2025 results were driven by a focus on fundamentals — core deposit growth to support loan expansion, positive operating leverage, disciplined credit management and healthy liquidity and capital ratios,” said Chairman and CEO Jim Ryan.

Old National settled the scale question years ago. What remains open is whether a $72 billion bank with a trimmed branch count can maintain the kind of commercial relationships that keep deposits sticky in a city that still prefers to know its banker.

Centier’s answer to consolidation is a promise not to sell

Indiana’s largest private, family-owned bank — now in its sixth generation of Schrage family ownership — has made a deliberate practice of being the institution that does not get acquired. On Feb. 6, 2026, Centier announced a leadership transition to the fifth generation of family leadership, naming Chris Campbell, son-in-law of the Schrage family, as president. Centier Bank says publicly and repeatedly that it is not for sale.

Where First Merchants is integrating a $2.5 billion deal, Centier is consolidating its Lafayette footprint: in the summer of 2025, the bank moved its downtown branch and its Business, Mortgage & Investment Center under one roof at 201 Main Street, adding a drive-through and positioning the combined location as a full-service commercial hub.

Centier held $362.4 million in Tippecanoe County deposits across five branches as of June 30, 2025 — a 9.27% share, ranking it third in the county, according to FDIC Summary of Deposits data. At just over $10 billion in assets and $7.84 billion in deposits statewide, Centier is large enough to compete for sophisticated commercial relationships while maintaining the local decision-making model that defines community banking. Return on average assets ran 1.50% in the most recent quarter. The bank’s Texas ratio — a measure of how well capital and reserves cover problem assets — stood at 5.08%, elevated from the near-zero levels of 2024 but well within the range considered stable by industry analysts.

J.D. Power ranked Centier first in retail banking customer satisfaction in the North Central region — Indiana, Michigan, Ohio, Kentucky and West Virginia — in its 2025 study, its first-ever regional award in that category. American Banker has named it the best bank to work for in Indiana for eight consecutive years. Good commercial lenders and wealth managers are hard to find and harder to keep. Those rankings help.

Fountain Trust has never missed a year of profit

Away from Greater Lafayette’s commercial core, the Fountain Trust Company makes a different argument about what banking in this part of Indiana can look like.

Founded in Covington in 1903, Fountain Trust operates 16 locations across six counties in west-central Indiana, including three branches in Tippecanoe County. It has reported a profit every year of its existence. Its most recent call reportshows $854 million in assets, $757 million in deposits statewide, $66.4 million in Tippecanoe County deposits and a 1.70% county market share, a net interest margin of 3.80% — well above both the 3.31% industry average and the 3.77% community bank average reported by the FDIC for the fourth quarter of 2025 — and a return on equity of 14.8%.

Decisions, the bank says, are made at the branch or in Covington. There is no distant corporate office. Lending limits are calibrated to local relationships. The ICBA’s annual CEO survey has repeatedly found that local decision-making authority is among the most valued differentiators community bank leaders cite when describing what sets them apart from regional and national competitors.

Regions has been cutting branches everywhere. Not here.

Regions Bank operates four locations in Greater Lafayette. By branch count, it trails First Merchants' six locations and Centier's five locations, making Centier the market's second-largest bank by local branch presence. Its Lafayette Main branch on South Street has been serving the market since 1957, making it one of the longest continuously operating bank locations in the city.

That longevity exists inside a very large parent. Regions Financial Corp., headquartered in Birmingham, Alabama, carried roughly $160 billion in total assets as of mid-2025 and operates more than 1,200 branches across the South and Midwest. Lafayette is one small corner of a bank that generates more than $1.8 billion in quarterly revenue.

Its 2025 full-year net income available to common shareholders was $1.77 billion. Net interest margin ran 3.65% — above the national industry average — and the adjusted efficiency ratio of 51.6% reflects an institution that has spent years rationalizing its branch network, consolidating roughly 30% of its locations since 2014.

egions held $239.8 million in Tippecanoe County deposits as of June 30, 2025 — a 6.14% share, according to FDIC data. That rationalization is the context for Regions’ presence in Lafayette. Four branches in a mid-sized Indiana university market is a deliberate footprint for a bank this size, not a legacy overhang. Regions has not pulled back here. What it offers is national-bank scale — digital infrastructure, broader product shelf, larger lending limits — from branches that have been embedded in this community for nearly seven decades.

Horizon and 1st Source round out the mid-tier

Two Indiana-headquartered regionals hold meaningful positions in the Tippecanoe County deposit market that the branch count alone does not fully suggest.

Horizon Bank, headquartered in Michigan City, held $225.2 million in county deposits across four branches as of June 30, 2025 — a 5.76% share, according to FDIC data. With $7.5 billion in total assets and a footprint spanning northern and central Indiana, Horizon competes in Lafayette as a mid-sized regional with deeper Indiana roots than the out-of-state nationals but less local history than First Merchants or Centier.

1st Source Bank, headquartered in South Bend, held $125.6 million in county deposits across three branches — a 3.21% share. Founded in 1863 and still headquartered in the same city, 1st Source has built its Indiana franchise around commercial lending, specialty finance and private banking, and its Lafayette presence reflects a deliberate push into central Indiana’s fastest-growing markets.

The rest of the room

Fifth Third and Huntington each maintain a meaningful presence in Greater Lafayette, competing in a market where the largest depositor is already a national bank.

Fifth Third Bancorp — a Cincinnati-based regional with $225 billion in assets — held $161.8 million in Tippecanoe County deposits across two branches as of June 30, 2025, a 4.14% share. Huntington National Bank, headquartered in Columbus with $200 billion in assets and a dense Indiana footprint, held $188.9 million across two branches — a 4.83% share.

Their competitive pressure on the market is less about lending relationships than about deposit competition: both offer digital platforms, nationally advertised rates and brand recognition that community banks and regional institutions have to actively work against.

Smaller institutions tell a different side of the same story.

Industrial Federal Credit Union (IFCU) was founded in 1954 on the floor of the Ross Gear plant on Heath Street in Lafayette, by factory workers looking for somewhere to save and borrow. The name has outlasted the plant.

Today IFCU operates nine locations across Lafayette, West Lafayette, Frankfort, Delphi, Monticello, Crawfordsville and Covington, serves 31,838 members and holds more than $300 million in assets. Forbes ranked it the top credit union in Indiana in 2025.

Its membership is still rooted in the region’s manufacturing sector, the same employer base that anchors the economy the article has been describing throughout. When Subaru, Caterpillar or Wabash National expands a facility and hires several hundred people, a meaningful share of those workers will eventually walk into an IFCU branch.

Security Federal Savings Bank cannot be acquired. Founded in Logansport in 1934 and operating as a subsidiary of Security Federal Mutual Bancorp, it is one of a small number of remaining mutual savings banks in Indiana, owned by its depositors rather than shareholders, with no stock outstanding and no mechanism for a traditional acquisition.

With $458 million in assets and $39.7 million in Tippecanoe County deposits across two branches — a 1.02% county share — it competes in the market without being subject to the same consolidation pressures bearing down on investor-owned institutions. In 2024 the bank opened a new facility in Carmel, its most ambitious expansion yet, bringing its total to seven locations. A mutual bank cannot be bought. It can only choose to convert — a decision that, once made, cannot be undone.

State Bank opened a Lafayette branch in October 2022, its first location outside the Indianapolis suburbs. Founded in 1910 as a community bank in Hendricks County, it has spent the past several years extending its reach eastward, opening a Lafayette branch in October 2022. With $864 million in assets and $29.5 million in Tippecanoe County deposits — a 0.75% county share — it is a bank that has found its footing in the Indianapolis suburbs and is testing whether that formula travels.

Lafayette is the easternmost outpost in a network otherwise anchored firmly in Hamilton, Hendricks and Boone counties. Whether the market absorbs it or pushes back will say something about how much room remains for a well-capitalized suburban community bank in a market already crowded with them..

What’s driving the market

The economy underneath all of this gives the region’s banks reason for optimism. The conditions under which they have to act on it are more complicated.

Timothy Zimmer, associate professor of economics and finance at the University of Indianapolis and the author of Indiana University’s Kelley School of Business annual Lafayette MSA economic forecast, described the region entering 2026 with a mixed picture. Total nonfarm employment fell slightly in 2025, down roughly 1,188 jobs on an annualized basis, as the labor force softened in the second half of the year. Inflation remained stubborn. Trade policy uncertainty continued to affect manufacturing investment timelines.

But the structural facts are durable. Greater Lafayette carries 35,500 manufacturing workers across the eight-county region — 18,800 in Tippecanoe County alone — and the employer mix has been shifting toward higher-credential sectors: Subaru, Caterpillar and Wabash National joined by semiconductor-adjacent firms and advanced manufacturing entrants whose capital requirements and investment horizons are categorically different from the previous generation of plant expansions. Population growth is steady and projected to continue.

“The area remains anchored by Purdue University and a diverse offering of industries and businesses,” Zimmer wrote in the 2026 Indiana Business Review forecast. “Few areas boast a range of industries, technology and skilled labor like Lafayette, and this advantage offers resilience and a strong foundation for the metro.”

Sustained commercial activity generates sustained loan demand. It also generates the commercial complexity — larger deals, longer timelines, more sophisticated borrowers — that separates well-resourced lenders from those managing growth on tighter margins.

Mikel Berger, president and CEO of Greater Lafayette Commerce, the region's chamber of commerce and economic development organization, put it in terms that the institutions financing that growth would recognize. "Site selectors ask about labor, infrastructure, incentives," he said. "They also ask whether the capital is here to support growth over time. In Greater Lafayette, the answer is yes — and the number of institutions competing to provide it is part of why."

The banking stress of 2023, which rattled regional institutions nationally, seems distant in Greater Lafayette. The institutions serving this market are, by the numbers, well-capitalized, profitable and operating without the kind of credit deterioration that defined that period. The FDIC’s first-quarter 2026 profile found that the share of unprofitable community banks nationally fell to 4.9%, down from 7.4% the prior quarter. The American Bankers Association’s chief economist, Sayee Srinivasan, called the result evidence that “banks of all sizes have increased their footprint” while maintaining stable asset quality.

The challenge in Greater Lafayette is not stability. It is execution, whether the institutions positioned to serve one of Indiana’s most dynamic regional economies can manage higher funding costs, rising technology expenses and intensifying competition profitably enough to keep pace with the market they are financing. That market shows no signs of slowing.

| A guest post by

|